After colossal efforts from water companies and the regulator, was the result ever going to be thus, asks Tom Hall, Chief Economist at Aqua Consultants.

On one side are the need for many improvements over the next five years, not limited to:

- starting to tackle the pollutions crisis,

- improving supply resilience in the face of climate change and growth,

- continuing to drive leakage down,

- and returning mains renewal to pre-2015 levels.

Ranged against is widespread dissatisfaction with the sector from customers and politicians and the impact of higher investment on strained customer affordability. This means that PR24 was always going to be a difficult compromise: Ofwat had an exceptionally tough job balancing the competing factors.

Ofwat appears to have gone quite some way to compromising with the industry in its final determination (FD) after a rocky draft determination (DD) in the summer. It’s softened its approach in several key areas.

Smoothing the financials

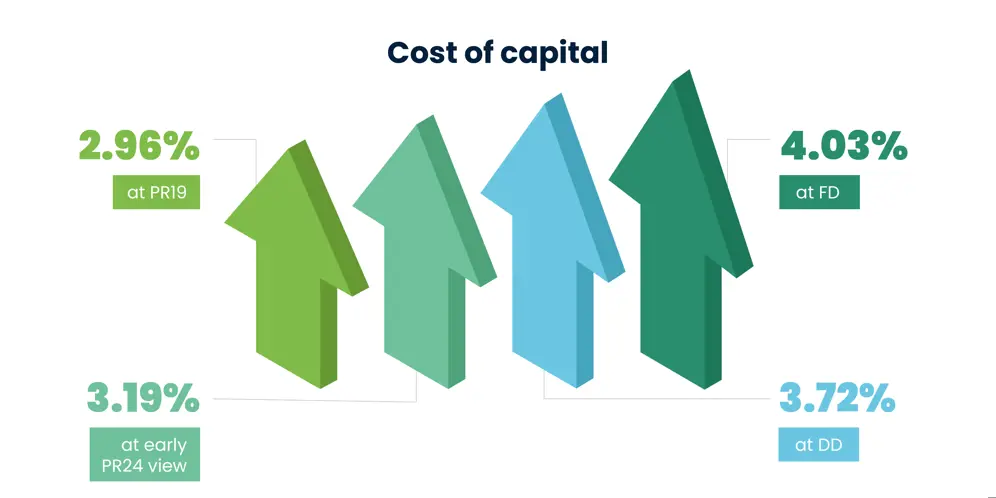

Firstly, risk and return: the cost of capital was probably the most contentious issue from the DD. Ofwat has landed on the highest point in its range, and has shown considerable movement over the process: from 2.96% at PR19 to an early PR24 view of 3.19%, to 3.72% at DD and finally alighting on 4.03%. Most of the movement is down to the higher cost of finance as interest rates have risen, but also no doubt reflects the need to continue to attract finance over the coming period.

However, a large gap still remains between companies’ and Ofwat’s view: many companies in their DD responses asked for 4.5% or higher. This is likely to be the key issue whether companies decide to roll the dice with a referral to the CMA: if they think they can win on the cost of capital, how close to the bone are their financials, and what return shareholders are willing to accept.

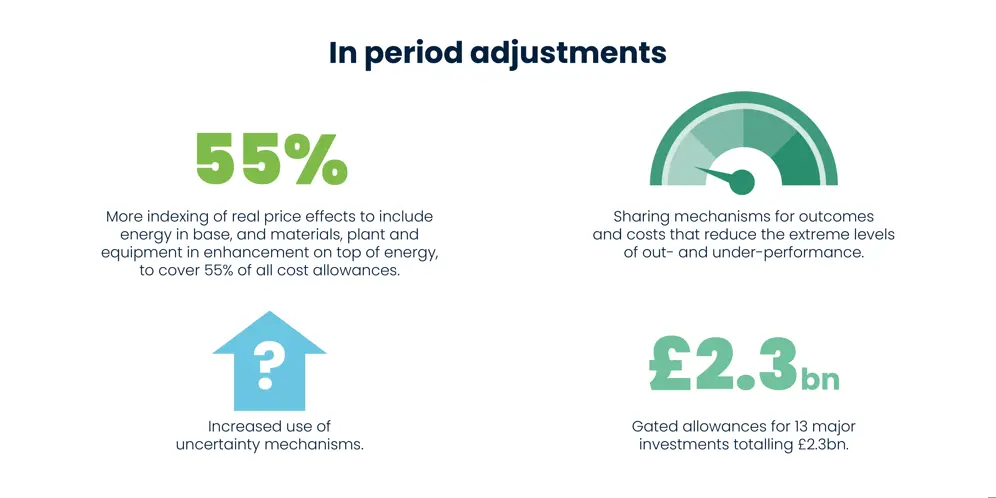

To sweeten the pill (and with a nod to the energy sector), Ofwat has also offered significantly improved in-period adjustments, with:

- More indexing of real price effects to include energy in base, and materials, plant and equipment in enhancement on top of energy, to cover 55% of all cost allowances.

- Gated allowances for 13 major investments totalling £2.3bn.

- Increased use of uncertainty mechanisms.

- Sharing mechanisms for outcomes and costs that reduce the extreme levels of out- and under-performance.

This all reduces the exposure to risk for companies, though this risk is passed onto customers. And uncertainty mechanisms can also work both ways: if the base assumptions are overly favourable, they could end up being negative adjustments. Nonetheless investors will be happy that any external shocks (such as the materials inflation seen post-Covid and the war in Ukraine) are likely to be less impactful moving forward.

Negatively for companies, Ofwat has held firm on its frontier shift adjustment of 1% per year. While this is more than in the past, it is consistent with other regulators’ recent approaches.

Outcomes

Ofwat has updated its outcomes for 2023-24, which gives a more pessimistic view of performance. It states that business demand is the only outcome to see a material change relative to DD.

The largest difference compared to the DD is the introduction of more caps, collars and deadbands to reduce risk to companies and customers from extreme under- and over-performance.

Expenditure allowances

In terms of expenditure, drawing firm conclusions over winners and losers is difficult as there have been many different stages of the process and companies adopt different strategies when putting their plans together: give up more to gain up-front rewards, or give up less in the hope that less will be cut out. Compared to their DD responses, the companies that have been cut the most are Wessex (-16.8%), Thames (-16.4%) and Sutton and East Surrey (-14.3%). Whereas a clutch of companies have been awarded slightly more than they requested or have only received a minor cut.

Overall Ofwat says that it has applied a 7% challenge to expenditure, up from 5% at DD – though because of higher company representations it has awarded an additional £16bn compared to DD. Wessex still has the largest cost-base gap, for some companies the gap has reduced at FD but for others significant gaps remain.

Asset health is another key area. Ofwat has held firm on its 0.3% per year mains renewal requirement, with some companies required to do significantly more from base expenditure. Welsh Water and Wessex received some additional allowances for base funding, but six companies need to do more than at DD. The big winners here are Welsh Water, who received an additional £144m. But they will still need to achieve 0.43% renewal rate per year. Ofwat’s average cost has increased slightly to £300/m but some will still feel this does not allow them to recover their costs.

The impact on bills

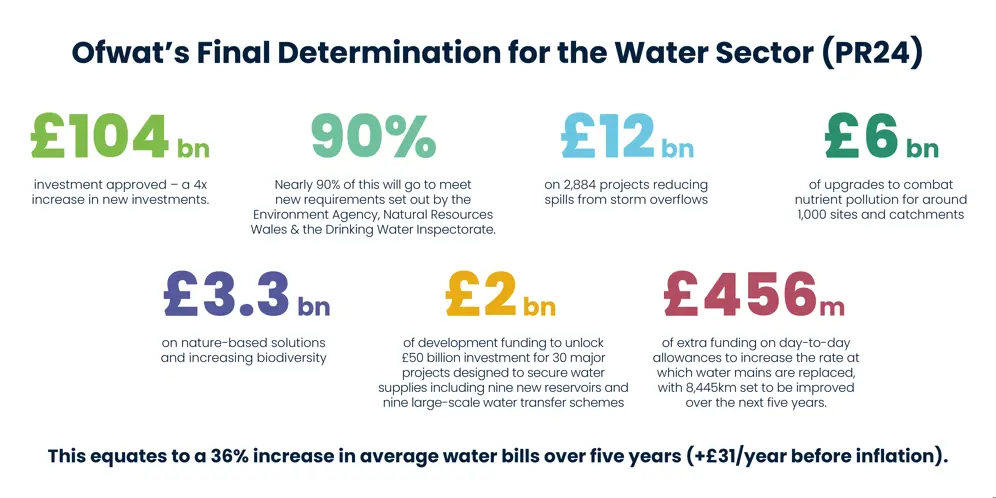

The result on customers of all of this is simple: bills are going to rise a lot over the next five years. Bills will be 36% higher for Water and Sewerage company customers in real terms by 2030, with large variations from company to company. Customers of Welsh Water, Severn Trent, Southern and Yorkshire Water will see rises of closer to 50% before inflation.

The compromise between more investment and higher bills is the lack of legitimacy of companies in many customers’ eyes, and without visibly improved culture and performance that is set to continue.

After the longest ever squeeze in incomes in recorded history, household finances are tight. Improving take-up of social tariffs will be key over the coming period.

Prognosis

Final Determination day is always a bittersweet day: it is the culmination of several years’ work, and there are always winners and losers. Great credit must go to companies and regulator staff for making it all happen.

What happens from here is uncertain: on first reading Ofwat has made some sizeable compromises compared to its DD: the likelihood of most companies appealing to the CMA has reduced. More than usual the decision will come down to the financials: are shareholders willing to accept the returns on the table, the lower risk from underperformance and higher cost gaps than previously. If not, PR24 will not be over for those companies.

The next five-year period will be pivotal for the industry: can it invest to cut pollutions, improve resilience, gain greater legitimacy with customers and ultimately put itself on a sustainable footing for the future. Customer bills will rise regardless. Companies that accept Ofwat’s determination will get a head start to solve these major challenges. The new year will tell us how many companies take the plunge with the CMA.